filmov

tv

genearlized autoregressive heteroskedasticity

0:40:31

GARCH: Generalized Autoregressive Conditional Heteroscedasticity | Time Series Lecture 17

0:05:10

What are ARCH & GARCH Models

0:21:00

15. Generalized Auto Regressive Conditional Heteroskedasticity (GARCH) in R || Dr. Dhaval Maheta

0:10:29

Time Series Talk : ARCH Model

0:09:02

R29 Intro to GARCH, Generalized Autoregressive Conditional Heteroskedasticity, , R and RStudio

0:05:14

Autoregressive Conditional Heteroskedasticity (ARCH) Model | Time Series forecasting

0:04:22

What Is the GARCH Process?

0:08:29

Generalization of ARCH: Theoretical introduction to GARCH

0:06:44

11.4.1 Models of Volatility Clustering - ARCH

0:08:20

Autoregressive conditional heteroskedasticity

0:10:25

GARCH Model : Time Series Talk

0:09:57

An Introduction to GARCH Models

0:20:25

Autoregressive conditional kurtosis (GARCHK): Time-varying heavy tails (Excel)

0:28:01

Time Series Analysis - Lecture 4: Conditional Heteroscedastic (ARCH) models

0:02:11

11.4.2 Models of Volatility Clustering - GARCH

0:25:31

ECON20110 Detecting Heteroskedasticity

0:04:11

Heteroskedasticity and Autocorrelation | Quantitative Trading Strategies and Models | Quantra Course

0:11:12

ARCH and GARCH Models

0:05:23

ARCH Models or Auto Regressive Conditional Heteroskedasticity Models | CFA Level 2

0:04:30

Autoregressive conditional heteroskedasticity | Wikipedia audio article

0:17:16

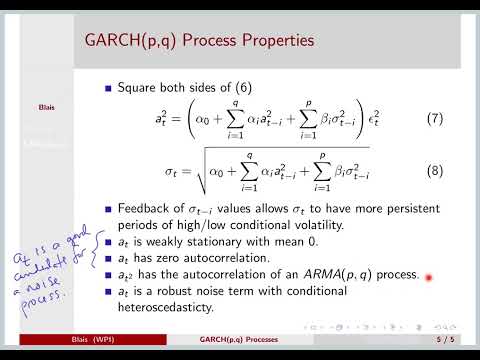

GARCH Processes

0:05:39

Overview of GARCH Models

0:12:40

Understand what are GARCH Models

0:10:39

Autoregressive Conditional Heteroscedasticity with Estimates of the Variances of UK Inflation Rates

Вперёд

0:40:31

0:40:31

0:05:10

0:05:10

0:21:00

0:21:00

0:10:29

0:10:29

0:09:02

0:09:02

0:05:14

0:05:14

0:04:22

0:04:22

0:08:29

0:08:29

0:06:44

0:06:44

0:08:20

0:08:20

0:10:25

0:10:25

0:09:57

0:09:57

0:20:25

0:20:25

0:28:01

0:28:01

0:02:11

0:02:11

0:25:31

0:25:31

0:04:11

0:04:11

0:11:12

0:11:12

0:05:23

0:05:23

0:04:30

0:04:30

0:17:16

0:17:16

0:05:39

0:05:39

0:12:40

0:12:40

0:10:39

0:10:39